How to Audit Your ABA Revenue Cycle in 30 Days

Most ABA organizations aren't facing a billing problem. They're facing a visibility problem — and the difference costs millions.

The Revenue You Don't Know You're Losing

If your ABA organization has never conducted a structured, end-to-end ABA revenue cycle management audit, there is a near certainty that you are leaking revenue — and the leak is bigger than you think.

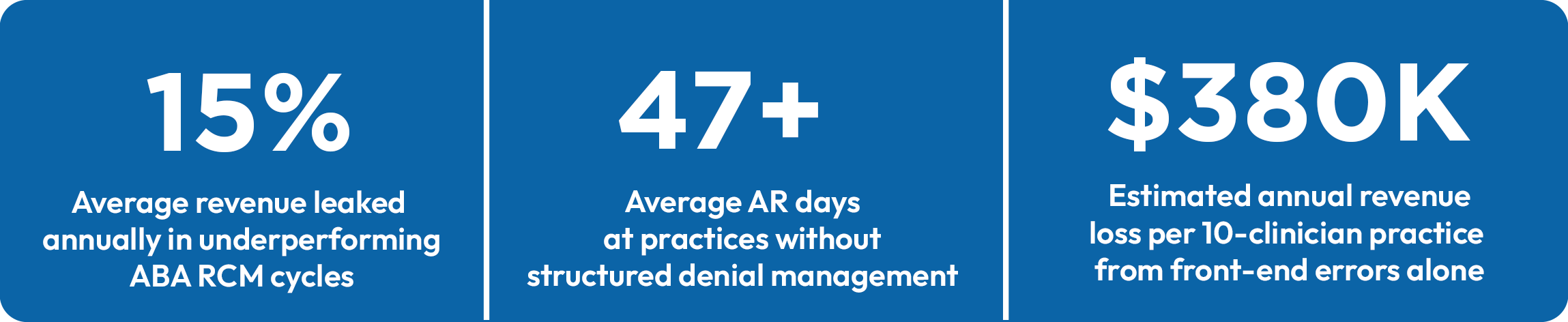

Industry data consistently shows that ABA practices operating without formal RCM oversight lose between 8% and 15% of collectible revenue annually. On a $5M practice, that is $400,000 to $750,000 walking out the door — often silently, across dozens of small failure points that no single report captures.

The problem compounds at scale. PE-backed platforms managing 10 or 20 clinic locations can carry tens of millions in preventable AR, claim rejections, underpayments, and authorization lapses — none of which surface cleanly on a standard P&L. What shows up is slower cash conversion, higher administrative cost ratios, and EBITDA that underperforms relative to session volume.

The hard number:

Authorization-related claim denials alone account for 23–30% of all ABA claim rejections (MGMA specialty billing benchmarks). Each denial costs an average of $25–$118 to rework — before accounting for the cash flow delay, which typically runs 45–90 days from original service date.

This guide introduces a structured 30-day audit framework for ABA operators, CFOs, and RCM leaders who need to diagnose revenue cycle performance quickly. Whether you manage ABA billing services in-house or are evaluating ABA billing outsourcing, this is a working playbook — not a theoretical overview.

Why Most ABA Revenue Cycle Audits Fail

The typical RCM audit in an ABA organization does one of two things: it reviews aged AR, or it looks at the denial rate. Both are useful. Neither is sufficient. Here is why most internal audits fail to expose root-cause revenue leakage:

- They start at the back end and work backward

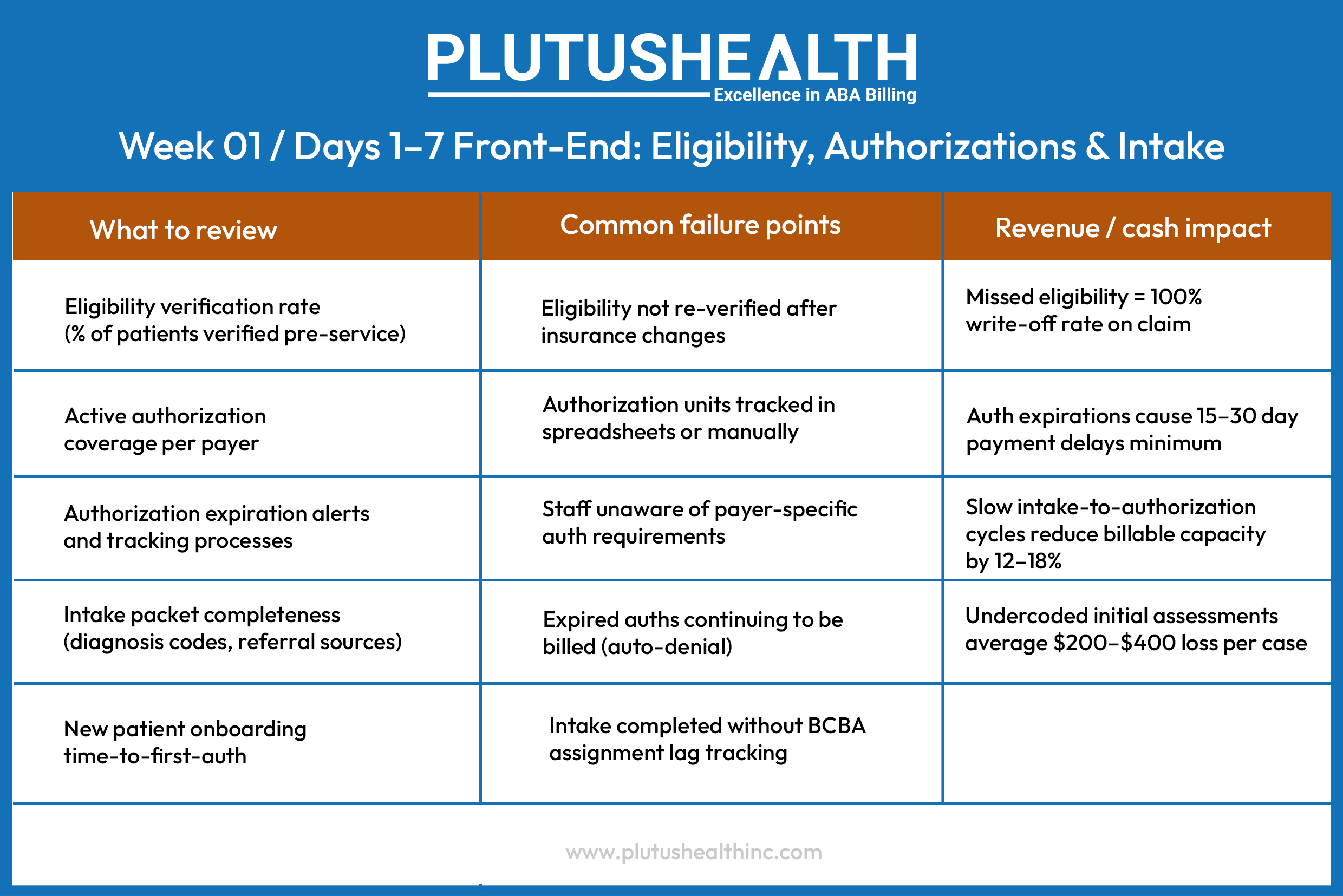

Reviewing aged AR tells you what already went wrong — not why it keeps happening. When a practice discovers $800K in AR over 90 days, the instinct is to chase collections. The correct response is to identify the front-end failure that put those claims in jeopardy in the first place. - They ignore front-end workflows entirely

Eligibility verification, prior authorization management, and intake accuracy are revenue cycle functions — not administrative tasks. In most practices, they are owned by non-billing staff with no RCM accountability. Errors made at intake rarely surface until 30–60 days post-service, when they become denial statistics. - They lack end-to-end workflow visibility

ABA billing involves a unique combination of authorization unit management, session note compliance, and behavior-specific CPT codes (97151–97158, 0362T, 0373T) that most general RCM frameworks were not built around. Audits that apply generic healthcare metrics miss ABA-specific failure modes entirely. This is why many organizations turn to a dedicated ABA therapy billing services company. - They produce a snapshot, not a system diagnosis

A point-in-time denial report does not capture cyclical patterns — authorizations expiring on the same day each month, a specific payer that routinely downcodes H0031, or a clinician whose session notes fail medical necessity documentation standards. Revenue leakage in ABA is almost always structural.

The core insight:

Revenue cycle audits fail because they measure symptoms, not systems. The 30-day framework below is designed to reverse that — building a full-cycle diagnostic that maps failure points to their source, not their consequence.

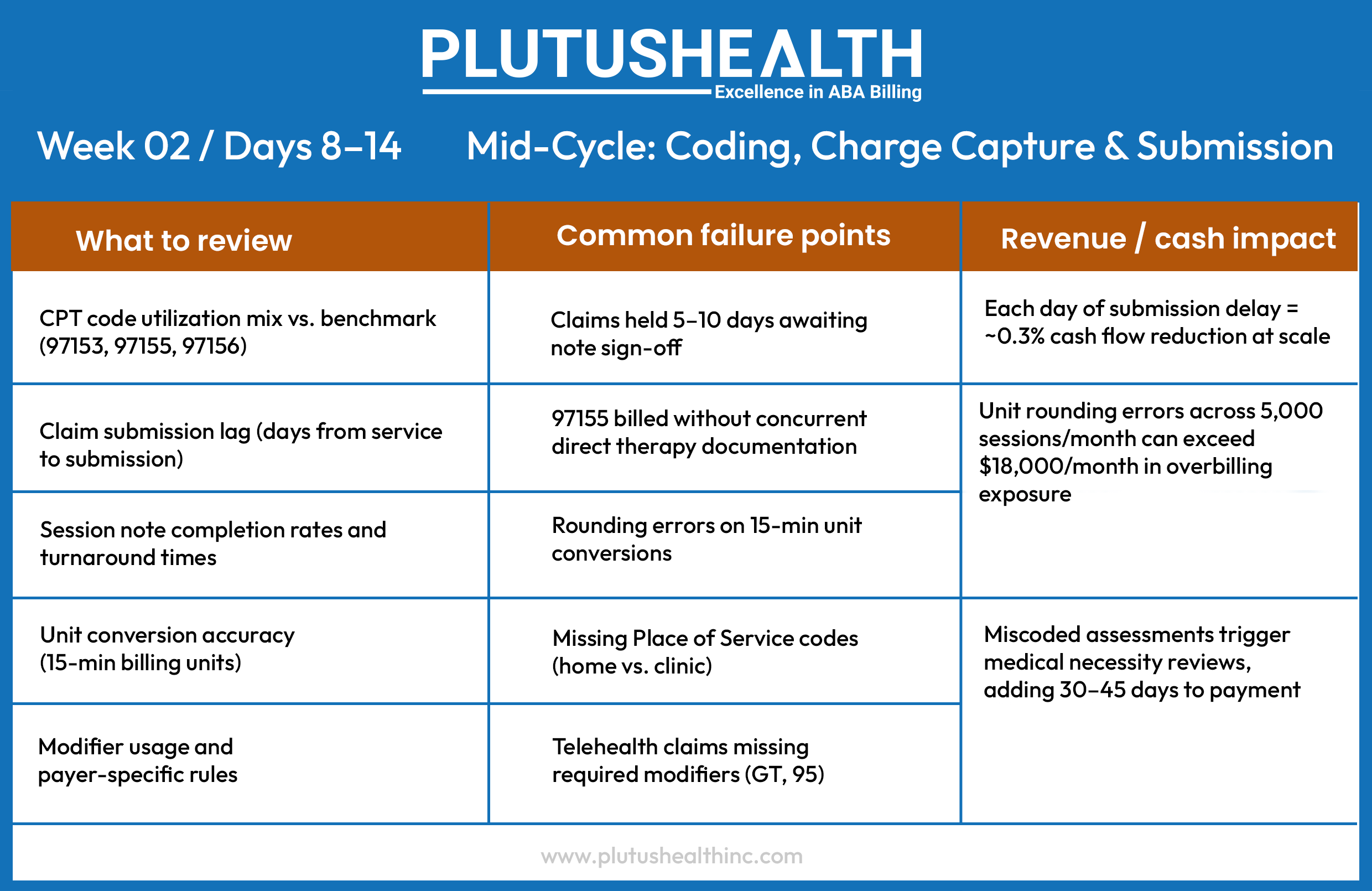

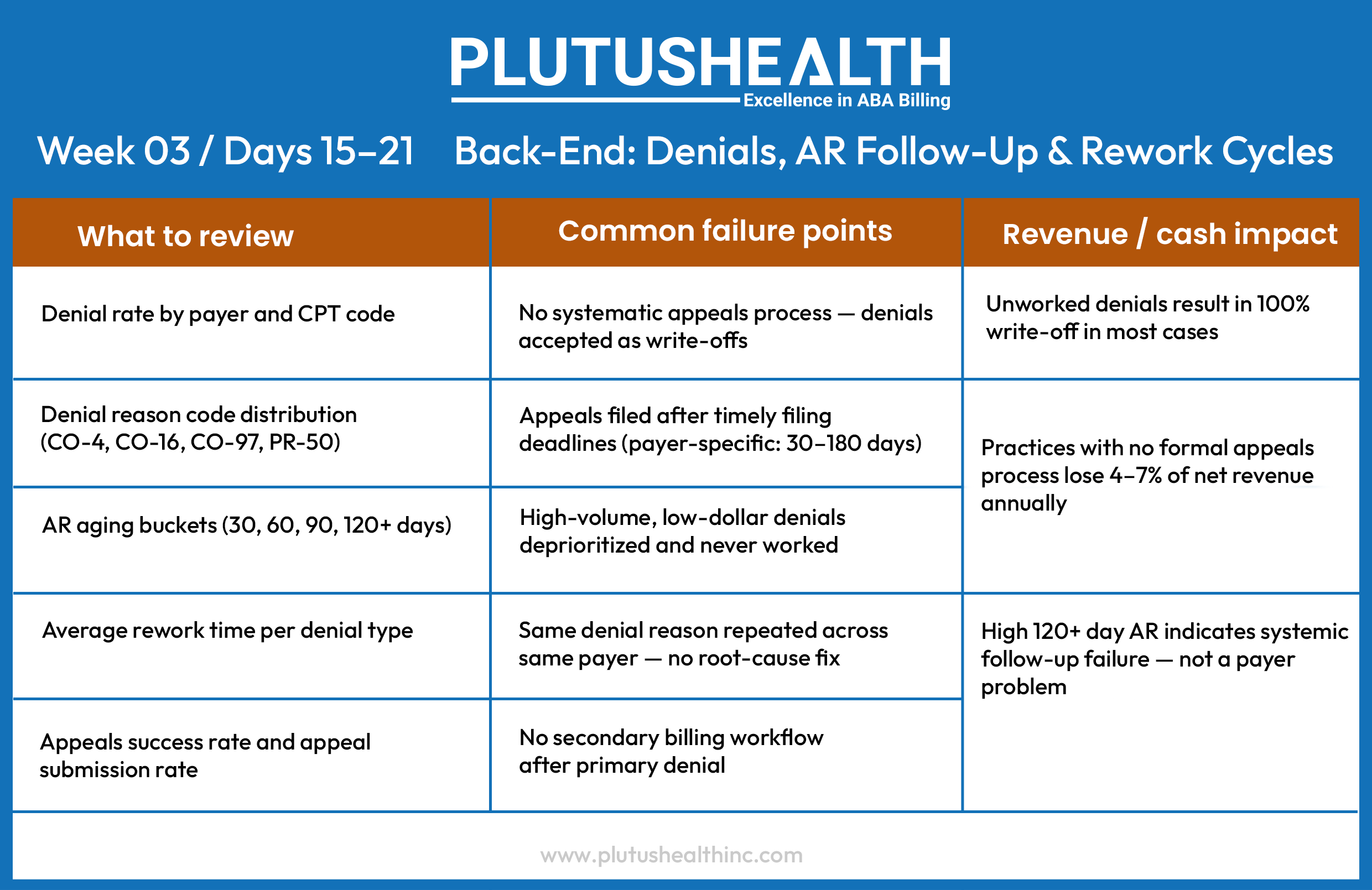

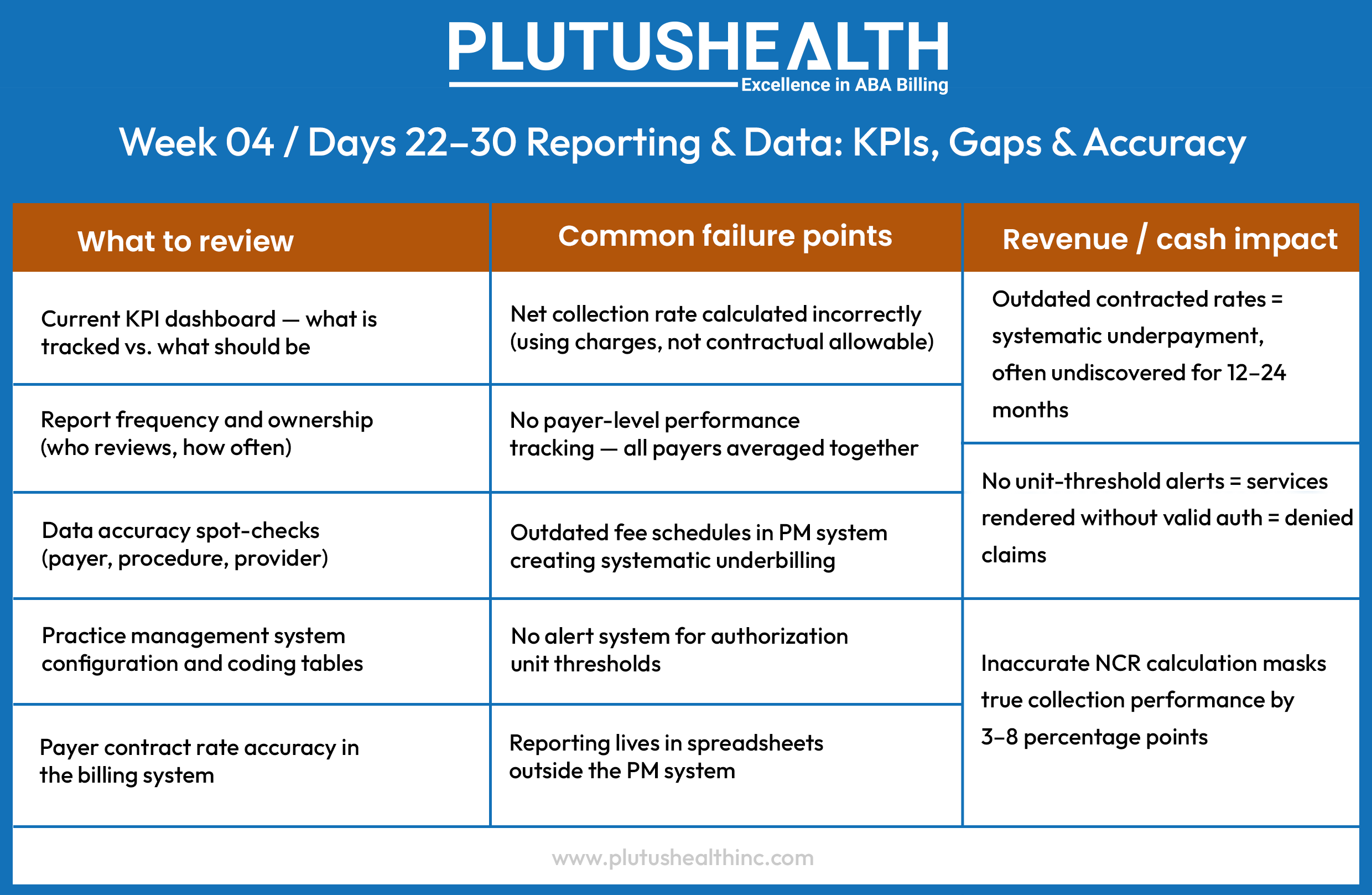

The 30-Day ABA Revenue Cycle Audit Framework

This framework is structured across four sequential weeks, moving from front-end intake through mid-cycle operations, into back-end recovery, and closing with data infrastructure. Each phase builds on the last — the findings from Week 1 directly inform where to look in Week 3.

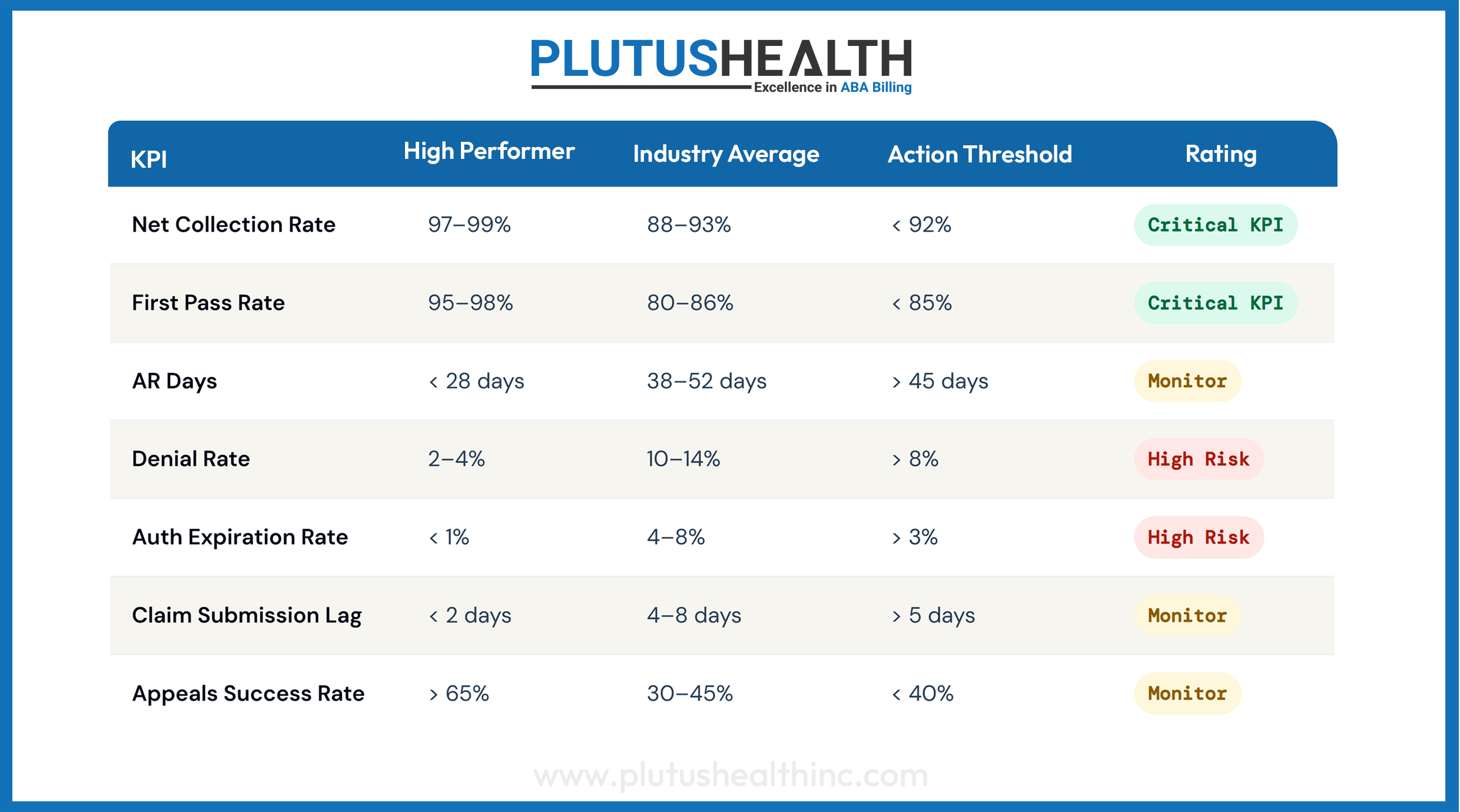

The Four Metrics That Define ABA RCM Performance

Revenue cycle performance in ABA is ultimately measured by four numbers. If you do not know your current performance on all four — whether managed through outsourced ABA billing services or an in-house team — you do not have a clear picture of your financial health.

Benchmark Ranges for High-Performing ABA Organizations

Use these thresholds as your audit scoring criteria. Leading ABA insurance billing services providers and in-house RCM teams alike are held to these standards by sophisticated acquirers and PE platforms during quality of earnings diligence.

Six Mistakes That Undermine the Audit

Even well-intentioned audits produce bad outputs. These are the mistakes most commonly made by internal RCM teams and general healthcare consultants unfamiliar with ABA-specific billing dynamics.

- Using gross charges to calculate NCR

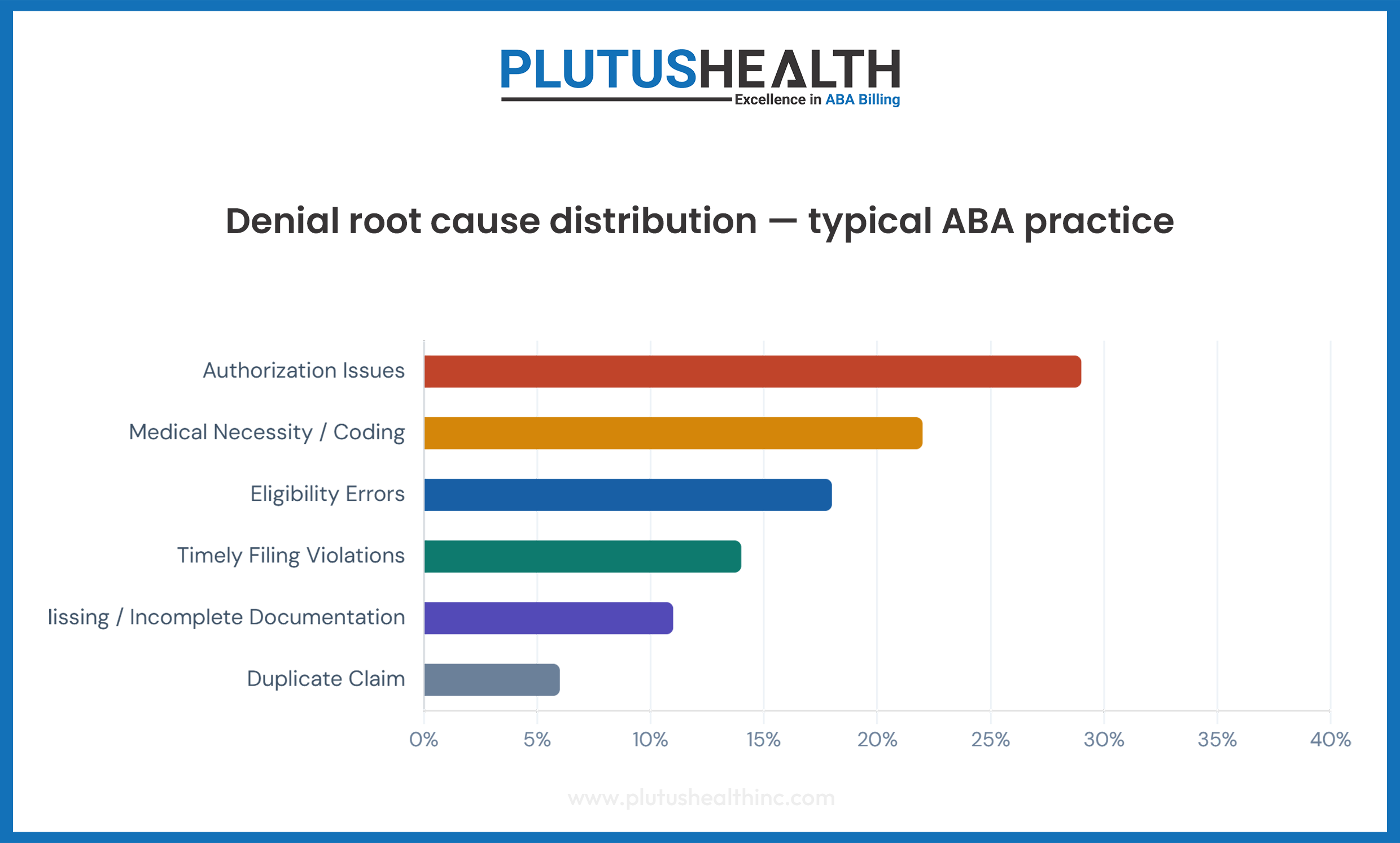

Net Collection Rate measured against gross charges is meaningless — it conflates contractual adjustments with collection performance. Always calculate NCR against contractual allowable. This error alone can inflate your perceived NCR by 15–25 points. - Averaging denial rates across all payers

A blended 8% denial rate may be hiding a 22% denial rate from Medicaid and a 3% rate from BCBS. Payer-level granularity is not a nice-to-have — it is the only way to identify targeted intervention points. - Benchmarking against general healthcare, not ABA

A 10% denial rate would be acceptable in many specialty areas. In ABA, it is a red flag. Authorization management, session note compliance, and treatment plan requirements create unique billing complexity that general RCM benchmarks do not account for. - Auditing a single month's data

Seasonal patterns, authorization renewal cycles, and payer contract changes create variance that single-month snapshots obscure. Audit a rolling 90 days at minimum — and flag any months that had unusual payer activity or staffing changes. - Ignoring the authorization-to-session utilization ratio

Many practices leave 10–20% of authorized units unbilled — not because services were not delivered, but because scheduling inefficiencies and attrition left units on the table. This is pure revenue that has been pre-authorized and pre-approved but never collected. - Not assigning an owner to each finding

An audit without accountable remediation owners is a documentation exercise. Every finding from the 30-day audit should map to a specific process owner, a corrective action, and a 60-day reassessment date.

What This Looks Like in Practice

Scenario · Mid-size regional ABA platform

The $1.2M Visibility Gap

A PE-backed ABA platform with 14 clinic locations and approximately $18M in annual revenue engaged in a revenue cycle review ahead of a follow-on capital raise. Their internal billing team reported an 89% collection rate and an average AR of 42 days — numbers that appeared functional on the surface.

The 30-day audit revealed a different picture. Authorization tracking was managed across three separate spreadsheets maintained by clinic-level office managers, with no central oversight. Across the network, 6.2% of billed claims were submitted against expired authorizations — resulting in systematic auto-denial. The appeals process for these denials was informal and inconsistent; less than 30% of appealable claims were ever resubmitted.

Separately, submission lag averaged 6.8 days — primarily due to a note sign-off bottleneck at the BCBA level — and the practice was calculating NCR against gross charges rather than contractual allowable, overstating collection performance by 11 percentage points.

Result: The audit identified $1.2M in recoverable revenue through a combination of retroactive appeals (within timely filing windows), process correction on auth tracking, and renegotiated payer terms on two underpaying managed care contracts. The authorization workflow was centralized and automated within 45 days of audit completion.

This scenario is not exceptional. It is representative of what a structured audit typically reveals in organizations that have grown rapidly without ABA revenue cycle management infrastructure scaling at the same pace. Many platforms eventually transition to outsourced ABA billing services precisely because this level of structural oversight requires dedicated specialization.

The Real Diagnosis: A Visibility Problem

The ABA organizations losing the most revenue are rarely billing the wrong codes or missing obvious errors. They are operating without the structural visibility to know where their cycle is breaking down — until the damage has already accumulated.

The 30-day framework above is built on one fundamental principle: revenue cycle problems in ABA are almost always process problems masquerading as billing problems. The denial is the symptom. The expired authorization, the unsigned note, the outdated fee schedule, the manual tracking spreadsheet — those are the cause.

For operators building toward scale, acquisition, or institutional partnership, this visibility problem carries real valuation risk. Sophisticated acquirers and PE platforms scrutinize net collection rate, AR aging, and denial rate as part of standard quality of earnings diligence. Whether you work with an ABA billing services company or manage an internal team, RCM performance that looks acceptable on a surface read often reveals structural fragility under that scrutiny.

The 30 days you spend on this audit will tell you more about your organization's financial health than the previous 12 months of standard reporting. More importantly, it will give you a clear map of exactly where to intervene — and what it is worth to fix it.

Final benchmark:

A high-performing ABA revenue cycle — NCR above 97%, denial rate below 5%, AR under 30 days, and first-pass rate above 95% — is not exceptional. It is achievable with the right process architecture. The question is not whether your organization can get there. The question is how much you are leaving on the table every month until you do.

Ready to Know Where You Stand?

If this audit framework surfaces questions about your current revenue cycle performance, the next step is a structured assessment — not a sales call. We work with ABA operators to identify and quantify revenue leakage, build RCM performance baselines, and design remediation roadmaps that deliver measurable results.